March Market Update 2026

This month we discuss the fallout from US and Israeli strikes on Iran, the effective closure of the Strait of Hormuz, and the market consequences of an oil shock that has left few places to hide.

As we move through the second half of 2024, the private market landscape continues to evolve, with the industry grappling with a difficult fundraising environment, ageing un-exited assets, and higher interest rates. Despite these challenges, market participants remain cautiously optimistic as sponsors or general partners (GPs) recalibrate and adapt to the changing environment.

For limited partners (LPs), however, the signals can feel mixed. Does this renewed optimism mark a turning point for the industry or a temporary respite?

To provide clarity amidst the noise, Neil Benjelloun, Senior Vice-President of Private Markets at Bedrock, has identified six key trends shaping the market today and in the near future. These insights, drawn from our direct experience as allocators to private market funds and co-investments, as well as Neil’s experience hosting educational Q&A sessions with leading fund managers, highlight both the challenges facing the industry and the opportunities on the horizon.

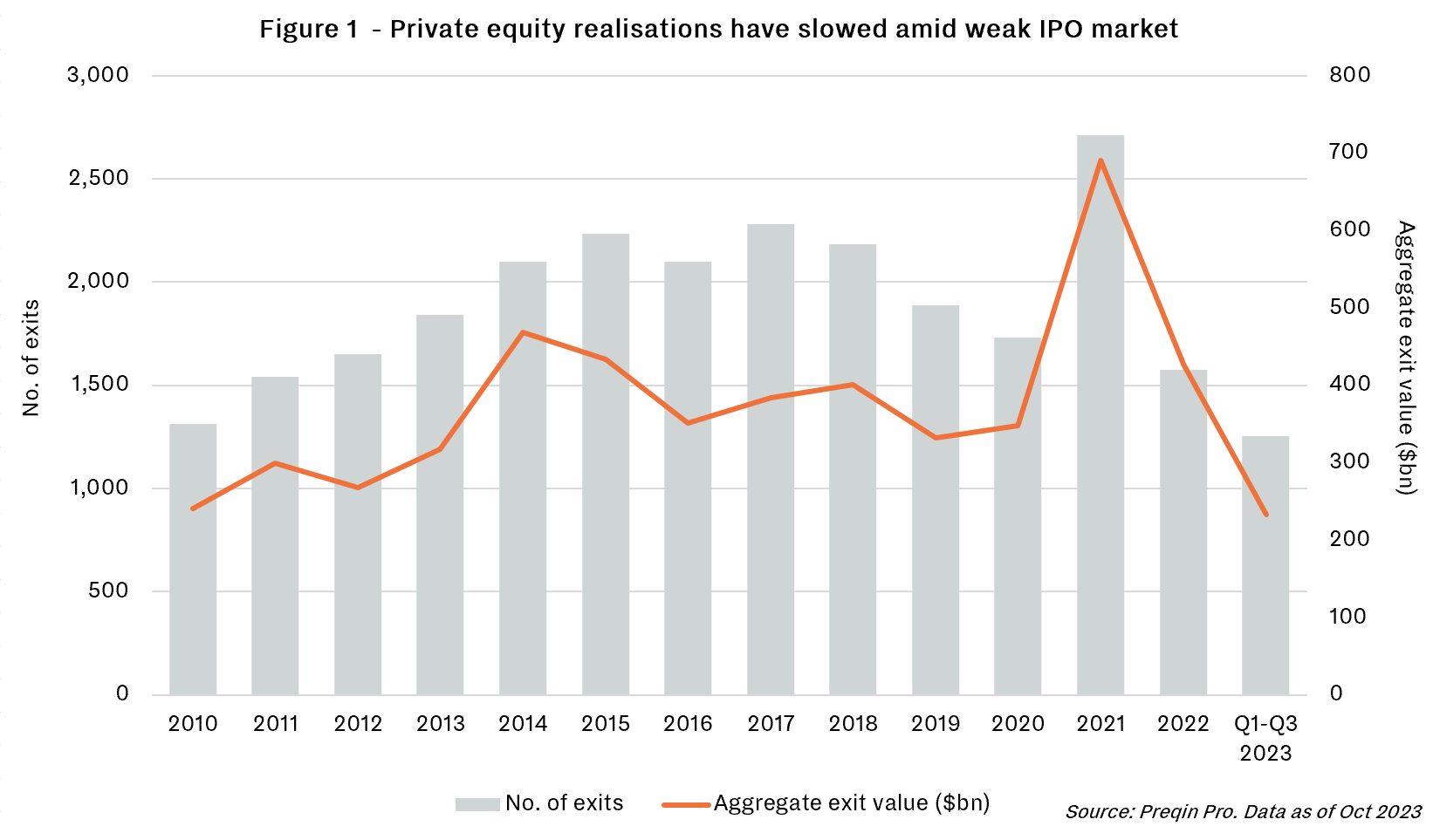

As indicated in Figure 1, a significant issue in the industry today is the growing backlog of ageing, un-exited portfolio companies, causing cash-strapped LPs to hold back on new private equity commitments until older assets are liquidated. Around 28,000 companies, worth between $3.2 and $3.4 trillion, are currently held in private equity funds, and nearly half of these assets have been held for over four years—the largest share since 2012. Exits have been slow to materialise as IPO markets have been virtually closed for most of the last three years, and rising interest rates have made LBO debt increasingly scarce.

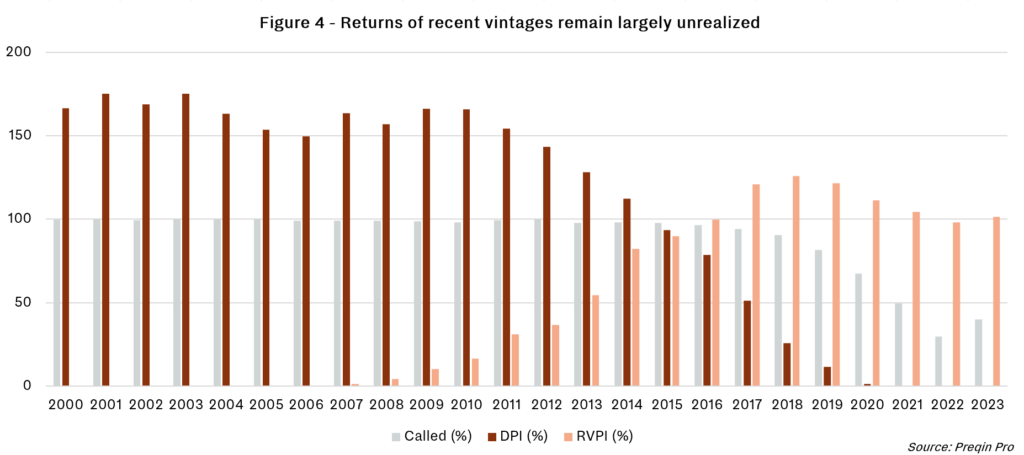

For instance, 2018 vintage funds are trailing by about 60% on a Distributions to Paid-In (DPI basis, with distributions over the past two years falling to around 12-13% of NAV annually, down from the historical 20-25%. GPs are turning to capital solutions such as dividend recapitalisations and GP-led secondaries to unlock capital and maintain fundraising momentum. The IPO market is showing signs of recovery, with public listings such as Arm, Reddit, and Stripe providing a glimmer of hope for 2024 and 2025 vintages.

While higher interest rates benefit direct lending funds, as the majority of their loans are floating rate, their pipeline of borrowers is increasingly filled with “good businesses with a maths problem.” Despite the strengths of these companies, the higher cost of borrowing and slow growth are straining balance sheets.

Over 90% of the direct lending market is dominated by covenant-lite (cov-lite) documents, with large funds compromising on lender protections to deploy record amounts of capital in this higher rate environment. Despite the capital influx, financing leverage-dependent buy-and-build strategies is becoming more difficult, and capital is increasingly reserved for larger, sponsor-backed deals. LPs must be more selective when deploying capital, especially when high single-digit to low double-digit returns are available through public market equivalents like fixed income.

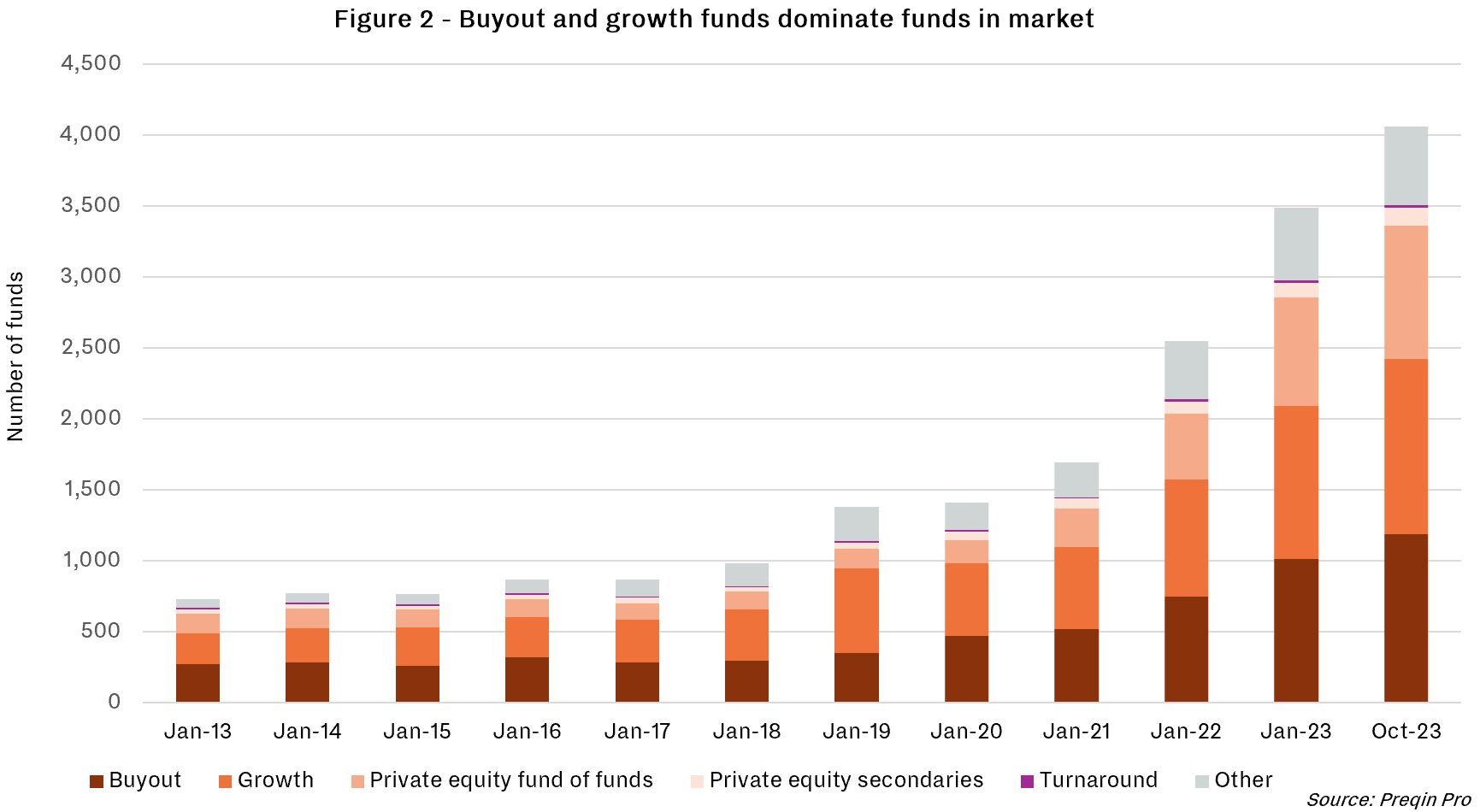

While overall fundraising has slowed, with 2024 seeing the lowest private capital raise since 2018, larger funds continue to thrive. Buyout funds raised 18% more year-on-year in 2023, with more than half of that capital going to the top 20 funds. This trend towards fewer but larger funds has persisted into 2024, reflecting growing market concentration.

Despite the tough environment, GPs are optimistic about tapping into private wealth, an area historically under-allocated to private markets compared to institutional investors. As more private wealth flows into private equity, larger funds are well-positioned to benefit from this shift.

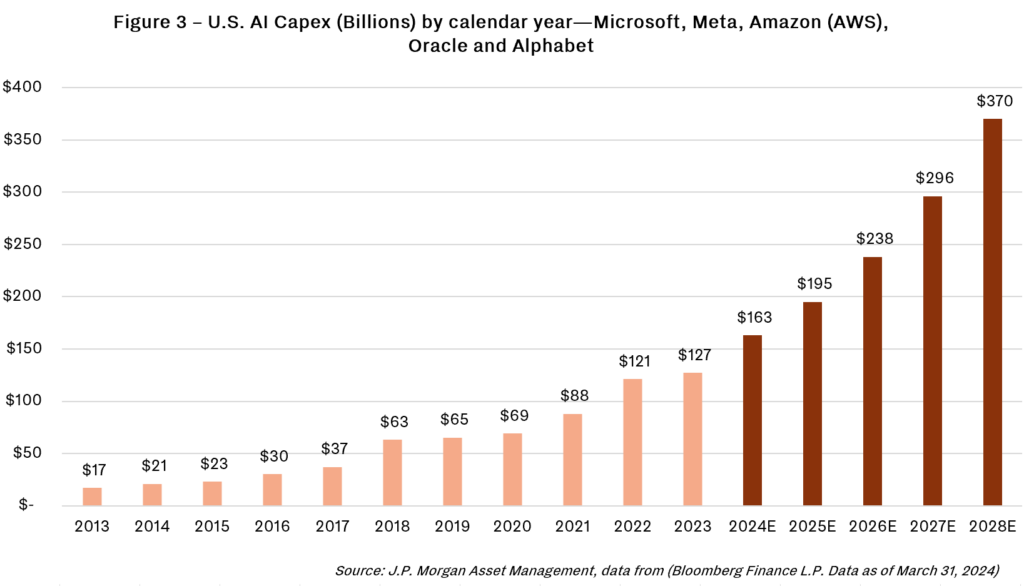

Artificial intelligence (AI) is emerging as a transformative force in private markets, with investors seeking exposure through themes like digital infrastructure and data centres. AI is reshaping investment processes, improving underwriting and due diligence, and amplifying tech talent within portfolio companies.

Forward-thinking investors are already leveraging AI to drive efficiencies, reduce costs, and unlock new growth opportunities. AI’s long-term potential, particularly as a disinflationary force, could significantly alter the private equity landscape, especially in sectors requiring large capital investments.

The private equity industry is increasingly focusing on niche areas such as infrastructure secondaries, NAV financing, and GP stakes, as LPs seek liquidity. GP stakes, in particular, are gaining popularity as they offer characteristics similar to various private market strategies: credit-like current income, diversification, exposure to mature funds, and potential equity upside akin to growth equity or venture capital. However, LPs remain cautious, as the exit environment for GP stakes is still unproven.

There is growing consensus that 2024-2025 buyouts could be the best vintages of the next decade, particularly when compared to 2017-2021 vintages. With more disciplined underwriting and a hands-on approach to portfolio management, the exuberance of the 2021 market has given way to more calculated investments. As easy returns, driven by cheap debt and high purchase multiples, fade away, value investors prepared to roll up their sleeves will find excellent opportunities. The focus is shifting back to basics, with emphasis on investment prices, value creation, and exit strategies.

While the private market faces significant headwinds—such as aging assets, rising interest rates, and concentrated fundraising—investors should take note of the emerging opportunities that have the potential to reshape the landscape. AI is not only revolutionising operational efficiencies but also enhancing decision-making processes, allowing firms to identify and act on undervalued assets more quickly. Niche strategies like GP stakes are gaining traction, offering investors unique exposure to high-performing managers, while buyout funds in the 2024-2025 cycle are projected to deliver strong returns, particularly as valuations stabilise.

To fully capitalise on these opportunities, it’s essential to partner with a manager who has the access, insight, and expertise to identify firms poised for sustained growth. Those that embrace innovation, investment discipline, and strategic capital management will be best positioned to navigate these changes and drive long-term growth.

If you have any questions about the private markets or the themes discussed in this article, please do not hesitate to get in contact with us, here.

Author: Neil Benjelloun, Senior Vice-President, Private Markets at Bedrock

Important Notice

This presentation is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security; nor does it constitute an offer to provide investment advisory or other services. Investing in private equities involves significant risks, including loss of the entire investment. For a detailed discussion on the risks involved, please refer to the ‘Disclaimer’ section on our website.

This month we discuss the fallout from US and Israeli strikes on Iran, the effective closure of the Strait of Hormuz, and the market consequences of an oil shock that has left few places to hide.

Bedrock has been named Best Independent Wealth Manager at the 2026 Euromoney Private Banking Awards, recognising the firms ability to combine independence with scale, sophisticated investment leadership, and a fully integrated multi‑family office offering.

Our Chief Investment Officer, David Joory, reflects on how rising oil prices, elevated volatility and shifting inflation expectations are shaping the current landscape.