Inside Private Credit: A Conversation with Greg Racz of MGG Investment Group

Posted by Bedrock on

To explore the evolution of private credit and its increasing role in financing, Neil Benjelloun, Bedrock’s Senior-Vice President of Private Markets, hosted a live Q&A session with Greg Racz, Co-Founder and President of MGG Investment Group. This discussion delved into the unique aspects of private credit, including its advantages over traditional lending models, market misconceptions, and emerging opportunities in the space.

Addressing the finance needs of the mid-market

MGG was established to address the needs of non-sponsored mid-market businesses that need flexible capital solutions.

Q [Neil]: Greg, can you start by sharing a bit about your background and what led you and Kevin [Griffin] to launch MGG?

A [Greg]: Sure. Big picture, what we do reflects 25-30 years at the senior level doing the same thing, helping finance the growth of US lower middle-market businesses, but with a focus on the non-sponsor side, meaning they don’t have a private equity backer arranging financing for them.

Kevin and I have been working together for almost 20 years. We launched MGG because we saw a gap in the market. Private credit was largely dominated by big firms catering to private equity sponsors, and we believed there was a huge opportunity to focus on non-sponsored businesses that need flexible capital solutions but don’t fit the typical PE-backed model. Today, over 80% of the investments we make in structured solutions and 100% of our flagship direct lending strategy are with family- and entrepreneur-owned businesses.

We focus on lower to middle-market businesses, typically in the $20-60 million EBITDA range, where banks have pulled back and larger private credit players don’t operate. This allows us to structure deals with strong lender protections and seek attractive risk-adjusted returns.

Differentiating from larger private credit players

A focus on non-sponsored lending, conservative leverage and strong covenants provides better pricing, less competition and stronger risk-adjusted returns.

Q [Neil]: How does your approach differ from the larger private credit firms raising and deploying multi-billion dollar direct lending funds?

A [Greg]: Most large private credit firms cater to private equity sponsors. Operating in the non-sponsored lending space provides three big differences (and advantages):

First, we’re much more aligned with the owners. These businesses are typically their most important asset, their “crown jewel”, not just one of many portfolio companies like in private equity. When PE firms own 15-20 companies, they’re comfortable maxing out leverage at 6-7x because they’re playing a portfolio game – some deals will do great, most will be fine, and the lenders take the hit on the ones that don’t work out. But for an owner-operator, this is their life’s work, so they tend to be more conservative with debt. That’s why we usually start with two turns less leverage, which should give us a bigger margin of safety on every deal.

Second, it’s a less competitive space, which means better pricing. Most private credit firms focus on sponsor-backed deals, and banks aren’t lending like they used to, so companies in the $20-40 million EBITDA range don’t have a lot of options. They’re too small for broadly syndicated loans or high-yield debt, and most private credit firms aren’t set up to lend outside of sponsor deals. That gap in the market allows us to command better spreads.

Third, the combination of lower leverage, strong covenants, and high cash yields makes a big difference. Because we keep leverage in check and focus on tight reporting and strong covenants, we avoid a lot of the risks that come with more aggressive capital structures. And since we’re highly selective with deals, we’re able to target strong risk-adjusted returns while still maintaining a solid margin of safety.

“These businesses are typically their most important asset, their “crown jewel”, not just one of many portfolio companies like in private equity.”

Looming maturity wall? The middle-market doesn’t care…

Every few years, people say there’s [a maturity wall] coming, but things always seem to work themselves out, and it hasn’t really impacted our opportunity set.

Q [Neil]: With refinancing pressure building over the next 18 to 24 months, how do you distinguish solid opportunities in non-sponsored deals from borrowers turning to direct lending as a last resort?

A [Greg]: I don’t put much weight on the idea of a maturity wall. Every few years, people say there’s one coming, but things always seem to work themselves out, and it hasn’t really impacted our opportunity set. Rates may not come down as fast as some expect, but that doesn’t change much for us either. There are always businesses in the lower and middle-market that need financing, regardless of the broader market environment.

In sponsor-backed deals, liquidity in the public markets can drive activity but also compress spreads. The larger private credit shops are more exposed to that dynamic. In our space, things are more stable. We focus on structuring loans with strong covenants and detailed reporting, which gives us early visibility into any potential issues. If a borrower is coming to us just because they can’t find capital elsewhere, that usually becomes clear in underwriting. We focus on businesses that make sense in any rate environment, not just when liquidity is tight.

Why borrowers choose non-bank providers

Structural changes in the banking sector mean non-bank lenders now service as the primary source of flexible capital for middle-market businesses.

Q [Neil]: Why should a borrower choose a non-bank lender? Do de-regulation and risk transfer strategies (e.g., SRTs) pose a competitive threat to private credit?

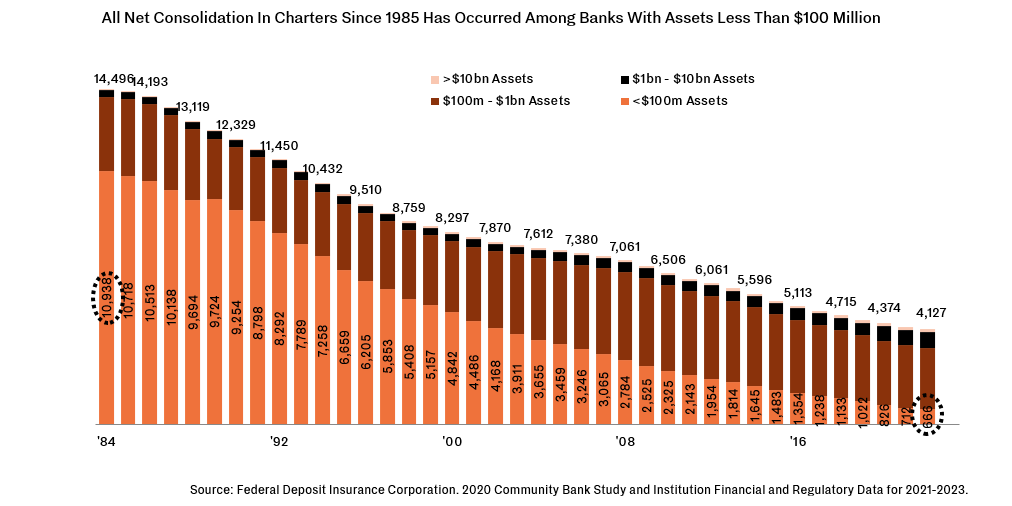

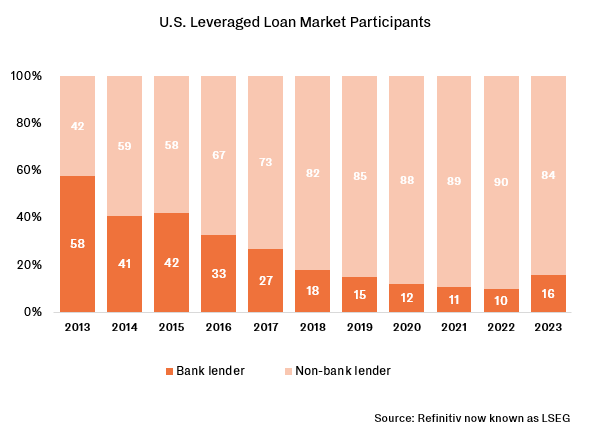

A [Greg]: Over the last 40 years, the number of small regional and community banks in the US has shrunk dramatically, limiting access to traditional bank loans for middle-market businesses. At the same time, deposits have moved into higher-yielding money market and brokerage accounts, reducing the amount of capital banks have available to lend. This has created a fundamental shift. Banks simply aren’t lending to these businesses anymore, leaving private credit as the primary source of financing.

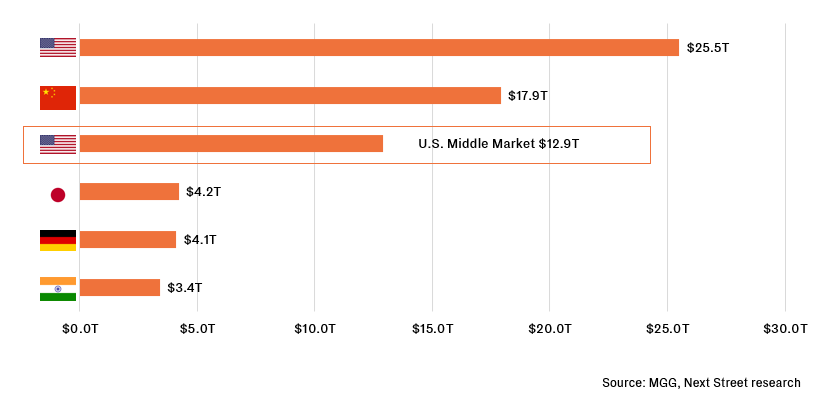

The US middle-market alone is massive, with hundreds of thousands of companies needing capital in both good and bad times (see chart below). Around 95 percent of these businesses are non-sponsored. A decade ago, many founders might have assumed they could just go to a bank for a loan, but that’s no longer the case. Now, most business owners understand that if they need flexible capital, private credit is where they have to go.

Some of the larger banks, like JPMorgan, have ramped up their private lending businesses, but they’re primarily focused on sponsor-backed deals or high-net-worth lending, not middle-market direct lending. SRTs, or synthetic risk transfers, are gaining traction, particularly in Europe, as a way for banks to offload credit risk and free up balance sheet capacity. But in the US, banks are still moving toward a narrow banking model, focusing on areas like private wealth, custody, FX, and investment banking that don’t require significant capital allocation.

Banks also have a fundamental structural challenge when it comes to lending. They operate at 12 to 15 times leverage, rely on customer deposits that can disappear overnight, and are ultimately backstopped by taxpayers. In contrast, private credit firms operate with no asset-liability mismatch, much lower leverage, and no reliance on government bailouts. This is why we believe regulators should favour private credit playing a larger role in lending, and it’s why we don’t see banks, despite SRTs or potential deregulation, as a major competitive threat to the growth of private credit.

Tackling industry misconceptions

Private credit is increasingly being recognised for offering lower leverage and fewer loopholes while avoiding the risk of high default rates.

Q [Neil]: What are the biggest misconceptions about private credit from founders and investors?

A [Greg]: Ten years ago, a lot of non-sponsored businesses didn’t even realise direct lending was an option. They just assumed banks were the only place to go for financing. That has changed as banks have pulled back from middle-market lending, and now most founders understand private credit is where they need to turn.

From an investor perspective, there is still this belief that sponsor-backed lending is inherently safer. In reality, sponsor deals tend to have higher leverage, sometimes six to seven times EBITDA, and default rates that are 50 percent higher. The reason for that is pretty simple. Sponsors play a portfolio game, so they push leverage as far as they can, knowing some deals will fail but the wins will offset the losses.

Beyond that, the way private equity firms have evolved liability management has made sponsor-backed lending riskier for creditors. If you look at the last decade, some of the most sophisticated PE firms have systematically structured credit agreements full of loopholes that let them shift assets away from lenders when things get tough. We have seen it over and over, from Caesars years ago to more recent cases like Pluralsight and Rackspace. Instead of putting in more equity to support a struggling business, sponsors are using those built-in optionality clauses to move collateral, extend debt, and avoid paying creditors.

Five years ago, investors were not paying much attention to this, but now they are starting to realise how much risk is embedded in these structures.

The role of covenants in risk management

Strong covenants remain essential for early risk detection and lender protection.

Q [Neil]: Some large shops seem to have conveniently forgotten that “covenants are the asset class” in private credit. What’s your take?

A [Greg]: Agreed, though I’d say it was more deliberate than that. The bigger credit funds made a conscious decision to loosen covenants because they needed to deploy capital. And so far, it hasn’t really hurt them, partly because the market bailed everyone out in 2020. But at some point, that strategy is going to catch up with them.

For us, having strong covenants isn’t about being predatory or trying to take over businesses. We’ve done 200 loans and only taken over four companies. That is a last resort. The real value of covenants is getting a seat at the table early. We deliberately set them tight enough to trip before real problems emerge, not after. If a borrower is supposed to hit $35 million in EBITDA and comes in at 33, we already have detailed monthly reporting that allows us to see it coming. We can have a calm, constructive conversation with management long before things spiral.

In the larger market, sponsors and bigger companies have more options. If they don’t like their direct lending terms, they can refinance with high yield, CLOs, or banks, often stripping out covenants altogether. We don’t do those deals. The ability to step in early, assess risk, and protect capital is what separates non-sponsor lending from the broader market.

“The real value of covenants is getting a seat at the table early.”

Q [Neil]: What challenges and opportunities do you see going forward, especially with Trump back in office and M&A activity still muted?

A [Greg]: Private credit does well in volatile environments, so it holds up through policy shifts and economic cycles. With Trump back in office, we’ll likely see financial deregulation that makes it easier for banks to lend. At the same time, his inflationary policies could keep interest rates higher for longer, which adds to economic uncertainty. That said, higher rates and tighter bank lending only increase demand for flexible financing.

On the M&A front, even with deal activity slowing, our pipeline has stayed steady because we’re not dependent on sponsor-driven transactions. We consistently close 15 to 20 deals a year, and when markets are uncertain, demand for structured solutions tends to rise as traditional financing gets harder to secure.

The biggest challenge in deploying capital right now is staying disciplined. There’s always pressure to chase volume, but we focus on our niche and make sure we do deep diligence, especially around second-tier management and tech infrastructure, which are often overlooked risks.

Looking ahead, private credit default rates are expected to rise, especially in highly leveraged sponsor-backed deals. But in non-sponsor lending, lower leverage and stronger covenants give us more control and let us step in early when needed. As banks keep pulling back from middle-market lending, private credit, particularly non-sponsor lending, will continue to be a key financing source.

“Higher rates and tighter bank lending only increase demand for flexible financing.”

Conclusion

Private credit continues to reshape middle-market financing, offering flexible capital solutions where banks have retreated. MGG’s focus on non-sponsored lending, conservative structures, and strong covenants aims to ensure resilience amid economic volatility. As private credit expands, disciplined underwriting and deep relationships will remain the foundation of sustainable success.

If you have any questions about the themes discussed in this article, please do not hesitate to get in contact with us at info@bedrockgroup.ch

Important Legal Information

This document has been approved and issued by Bedrock SA licensed under Swiss Law, authorised by the Swiss Financial Market Supervisory Authority (FINMA) and supervised by the AOOS – Schweizerische Aktiengesellschaft für Aufsicht, Bedrock Monaco SAM authorised and regulated by the Commission for the Control of Financial Activities (“CCAF”), and Bedrock Asset Management (UK) Ltd. authorised and regulated by the Financial Conduct Authority in the UK (jointly, hereafter, “Bedrock”).

The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice. This information contained herein is for the sole use of its intended recipient and may not be copied or otherwise distributed or published without Bedrock’s express consent. No reliance may be placed for any purpose on the information contained in this document or their accuracy or completeness. Information included in this document is intended for those investors who meet the Financial Conduct Authority definition of Professional Client or Eligible Counterparty or for those investors who meet the Swiss Federal Act on Financial Services Act (FinSA) of a Professional Client.

Confidentiality

The recipient will use this article for the sole purpose of obtaining a general understanding of the business, operations and financial performance of Bedrock in order to make a decision as to whether the recipient should proceed with a further investigation of the Funds and this investment opportunity. Bedrock reserves the right to request the return of this article at any time, without the retention of any copies by the prospective investor.

Investment risks

The value of all investments and the income derived therefrom can fluctuate due to market movements and you may not get back the amount originally invested. In the case of overseas investments, values may vary as a result of changes in currency exchange rates. This may be due, in part, to exchange rate fluctuations in investments that have an exposure to currencies other than the base currency of the portfolio. Past performance is no guide to or guarantee of future performance. The forecasts presented in this document are provided for illustrative purposes only and are not a reliable indicator of future performance.

Alternative investments risks in general

As a professional client, you should be aware that investing in alternative investments can carry significant risks. Alternative investments are investments that do not fall under the traditional categories of stocks, bonds, and cash. Examples of alternative investments include hedge funds, private equity, venture capital, and real estate.

Under the FCA financial promotions framework, alternative investments can only be promoted to professional clients, such as yourself. This is because professional clients are deemed to have the necessary knowledge and experience to understand the risks involved in these investments.

However, even with this level of expertise, it is important to be aware of the risks involved in alternative investments. Some of the risks include:

Illiquidity: Alternative investments can be difficult to sell quickly, which means that you may not be able to access your money when you need it.

Lack of transparency: Alternative investments are often less transparent than traditional investments, which means that it can be difficult to get a clear picture of the underlying assets and their performance.

Complexity: Alternative investments can be complex, with unique features and structures that may be difficult to understand.

Concentration risk: Alternative investments often require a large minimum investment, which means that you may end up with a concentrated portfolio and a high degree of exposure to a single investment.

Higher fees: Alternative investments often come with higher fees than traditional investments, which can eat into your returns.

It is important to carefully consider these risks before investing in alternative investments. You should also ensure that you understand the terms of the investment, including any fees and charges, before committing your money.

If you have any questions or concerns about investing in alternative investments, you should seek the advice of a professional financial advisor who is qualified to advise on these types of investments.

Limitation of liability and indemnity

Bedrock expressly disclaims liability for errors or omissions in the information and data contained in this document. No representation or warranty.

You agree to indemnify and hold harmless Bedrock and its affiliates, and the directors and employees of Bedrock and its affiliates from and against any and all liabilities, claims, damages, losses or expenses, including legal fees and expenses arising out of your access to or use of the information in this presentation, save to the extent that such losses may not be excluded pursuant to applicable law or regulation.

Any opinions contained in this presentation may be changed after issue at any time without notice.

Copyright and other rights

The copyright, trademarks and all similar rights of this presentation and the contents, including all information, graphics, code, text and design, are owned by Bedrock.

European defence stocks have soared since Donald Trump’s return to the White House. In this article, our Research Team explores how European defense equities are gearing up for increased investment and growth opportunities in the evolving security landscape.

This month we discuss the market volatility in March, the new US tariffs—both implemented and announced, developments in the Russo-Ukrainian war, the latest economic data, and the outlook for the almighty US dollar.

This month we discuss the violent equity rotation from the US and growth to Europe, EM, and value, America’s hard-line trade revisionism, falling bond yields, and developments in Ukraine.