Exploring the Energy Transition with Guinness Global Investors

Posted by bedrock on

Renewable energy stocks have been knocked in recent years by higher interest rates and other headwinds. But the energy transition – from a predominantly fossil-fuel economy to one electrified with renewables – has continued apace. In 2023, global renewable capacity installation grew at its fastest annual rate in two decades, while technological advances continue to make renewables cheaper and more efficient.

With interest rates coming down and the US election almost upon us, Tom Bayes, from Bedrock’s research team sat down with Will Riley and Jonathan Waghorn – managers of the Guinness Sustainable Energy Fund – to explore the state of the energy transition today, and opportunities for equity investors.

Guinness Global Investors is a London-headquartered long-only equity investment house with over 25 years’ experience investing in both incumbent and renewable energies (alongside other strategies, from equity income to Asian stocks). Will Riley and Jonathan Waghorn have managed Guinness’ Sustainable Energy Fund since 2019. They also manage the Guinness Global Energy Fund, investing in non-renewable energies.

Energy Transition: A Long Road Ahead

Q: [Tom] Where does the energy transition stand today? What progress has been made – and where do we go from here?

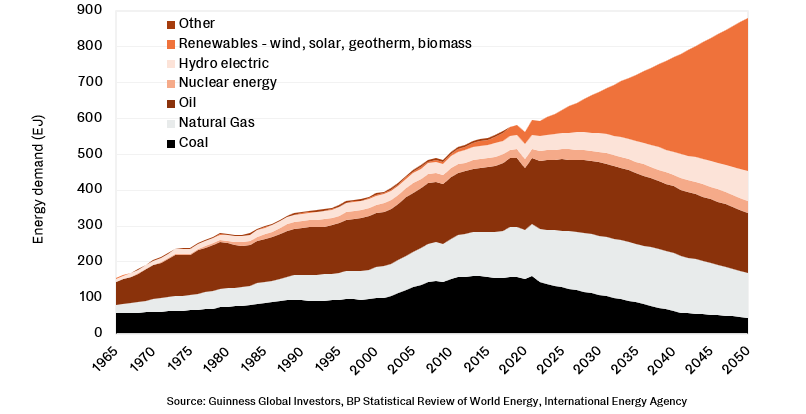

A: [Guinness] The quick answer is that it is going to be a long transition – some good progress has been made but there is a long way to go. Looking at the energy mix today, renewable generation is growing strongly but fossil fuels still dominate, accounting for around 83% of energy use. Based on our own modelling of a realistic base-case transition scenario – which draws on data of our current trajectory from the International Energy Agency and others – we see renewables supplying around 50% of world energy by 2050. So the transition still has a very long way to go. Coal will be the clear loser from the transition, whereas we see oil demand growing until 2030 and natural gas peaking around 2040.

Investment in clean energy was around $1.7 trillion last year – up about three times versus 2019. But it’s important to say that our base-case scenario is not the full Net Zero transition [i.e., net zero economy-wide carbon emissions] by 2050 needed to meet the Paris Agreement goal [to limit the global temperature rise to 1.5°C above pre-industrial levels]. Our scenario equates to around +2.3°C or +2.4°C of warming. For Net Zero by 2050, we would need to see more dramatic change in how we consume energy, a steeper reduction in fossil fuels, and annual renewable investments in the order of $4.5 trillion annually. We don’t see that yet. There is a danger of thinking +2.4°C of warming is a complete failure because it’s not within the 1.5°C Paris Agreement goal. But it is important to remember that as recently as 2016, when the Paris Agreement was signed, the business-as-usual scenario was for +3.5-4°C of warming. So really good things are happening – it’s just that this next bit does get harder.

“Investment in clean energy was around $1.7 trillion last year – up about three times versus 2019.”

Net Zero: Obstacles and Opportunities

Q: [Tom] What is the main bottleneck preventing Net Zero targets being reached?

A: [Guinness] We need investment in the transition to be much higher across the board. The US Inflation Reduction Act (IRA) is a huge step in making that happen. But it’s completely clogged up amid the US election uncertainty. Meanwhile, the EU has fallen behind the curve. Before, it was leading; now it’s all targets and hopes, with no real money hitting the road. China is going for it at tremendous scale, with a lot of state support.

For a full Net Zero transition, beyond adding renewable generation, we would need to reduce fossil fuel use faster. One thing you could do tomorrow to accelerate this reduction would be a carbon price of $150/tonne – for everybody. That would change behaviour in a real way. But a global carbon price is a long way off.

Russia’s invasion of Ukraine sharpened the focus on energy security and many countries are interested in reducing dependency on Russia and OPEC. This highlighted the value of sustainable energy sources, as every country has an opportunity to secure supply at home – be it wind, solar or another technology.

“The value of sustainable energy sources is that every country has an opportunity to secure supply at home – be it wind, solar or another technology.”

Looking Beyond Wind and Solar

Q: [Tom]How settled are the technologies that get us to the transition – is it all about solar photovoltaic and wind, or are other options in play?

A: [Guinness] We do expect wind and solar to dominate and we are continuing to see incredible efficiency and cost improvements. For example, Chinese firm Dongfang broke the record for the largest offshore wind turbine just last week, with 26MW capacity – smashing the 18MW mark set in June this year. But we’re not going to have a world that’s 100% wind and solar. The rule of thumb is you can comfortably get variable renewables to about 30-40% of energy supply in a typical economy. By adding storage – batteries, pumped hydro – you can push that up to 60-70%. But ultimately, the solution will involve a blend of technologies.

“With variable renewables (wind, solar) you can comfortably get to about 30-40% of energy supply. Adding storage – batteries, pumped hydro – you can push this up to 60-70%.”

There is a lot of talk about nuclear, especially Small Modulor Reactors (SMRs) and the interest from hyperscalers like Google. We see nuclear as part of the mix – but not a dominant part of it in 25 years’ time. Most of the existing nuclear plants worldwide are half a century old and getting to the end of their useful life, so a lot of future investment will simply go into replacing these and we do not expect a huge amount of net growth. On SMRs, the plans look great on paper – but commercialisation is enormously expensive. Look at NuScale, who got the first SMR permit in the US years ago. However, the timeline kept getting pushed back, costs soared, and backers ultimately pulled out. There are also other concerns, such as leakage from SMRs seemingly being higher than conventional nuclear plants, which will have to be addressed. So we don’t see SMRs being at a commercial scale until the mid-2030s.

Hydrogen has a similar story. The EU Green Deal in 2021 had big targets for European hydrogen demand by 2030, yet we are only at about 20% of that level now, hydrogen remains expensive (particularly green hydrogen, which is produced via electrolysis using renewable electricity), and battery EVs have stolen a march for light vehicles. We do still see hydrogen having a place in the energy mix, with interesting applications in energy storage, but it will be a smaller one.

Driving Transition Through Efficiency

Q: [Tom] There’s a natural tendency to focus on the generation of electricity – and the supply side generally. What is the role of efficiency and the demand side?

A: [Guinness] Efficiency is too often overlooked. The size of total energy demand will be crucial in managing the transition. Put simply, if you’re not using the energy in the first place, you don’t need to worry about where it came from. With populations and economies growing, energy use needs to become twice as efficient in the years ahead. That’s doable – and we see it across our investment universe. Investment in energy efficiency is accelerating and global energy intensity has improved. Investing in the energy transition is not just about wind and solar. It is also about efficiency solutions, especially in buildings – like insulation, efficient lighting and intelligent building products. Some of these may seem like boring companies but we see very attractive growth rates and market structures.

“Investing in the energy transition is not just about wind and solar. It is also about efficiency solutions, especially in buildings – like insulation, efficient lighting and intelligent building products.”

Electrification is also a big part of it, be it electrifying heating (with heat pumps) or transportation and industry. We’re used to thinking of hydrocarbons as very energy dense… which they are. But it’s a mistake to assume they are efficient. Eighty to 90% of energy is lost in an internal combustion engine. Battery power is less energy dense but much more efficient. We see investment opportunities across the supply chain, from battery metal miners, through EV component makers to EV assemblers.

Key Factors Shaping Clean Energy Stocks

Q: [Tom] Despite the activity on the ground, the last couple of years have been challenging for share prices in the space. Why is that?

A: [Guinness] There has been a laundry list of factors – higher interest rates, raw material inflation, US political uncertainty delaying IRA-linked investment, lower-cost Chinese manufacturing pressuring margins.

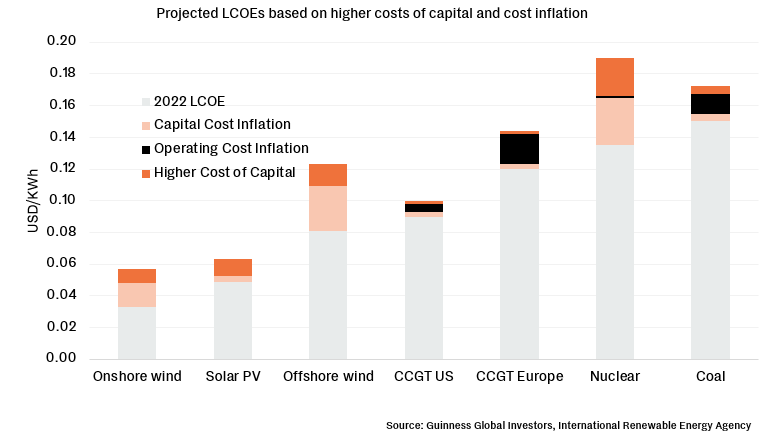

Renewable energy projects are highly interest rate sensitive, as the bulk of the cost is upfront capital investment – but projects run cheaply after that, as there is no fuel cost. For fossil-fuel generation, the inverse is true, with a much higher proportion of project costs related to operation (e.g., constantly buying the fuel). So rates going from near enough 0% up to 5% impacts the economics of renewables more. Higher rates also impact the demand side, as a lot of purchasing – for example, solar modules for your roof and EVs – is debt-financed. Clearly interest rates coming down can benefit renewables.

Raw material and supply-chain inflation hit margins, too. The price of lithium going from around $15,000/tonne to $70,000/tonne really did impact the economics. But the issue of inflation has started to roll over. It is also worth highlighting that Chinese competition – often state-sponsored and with lower cost of capital – has hit margins in certain parts of our universe, though other areas have seen no impact.

Q: [Tom] Do renewables need interest rates to come all the way down to pre-COVID levels to improve the economics – and market sentiment?

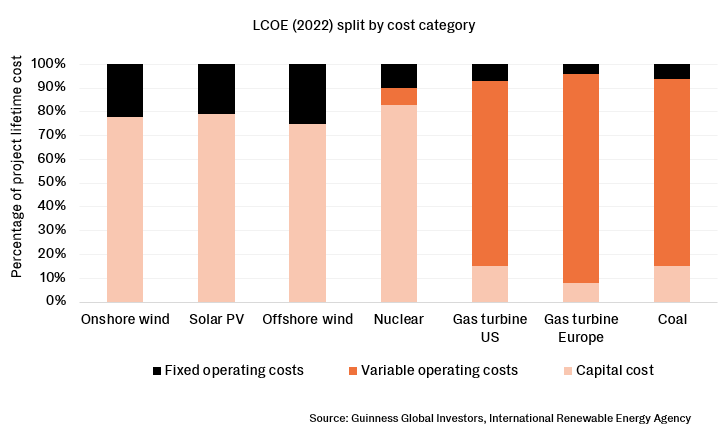

A: [Guinness] For all the increases in interest rates, the levelized cost of electricity (LCOE) of renewables actually fell in 2023 versus 2022, driven by technology and other efficiency gains. Even with the higher costs from inflation and higher rates, onshore wind and solar PV have remained cheaper than fossil fuel generation. This suggests that while interest rates are a factor, they are just one factor – and not necessarily the most important. The learning rate [at which technologies and processes improve, bringing costs down] for solar and wind has been steep – and we’re not at the limit yet. The learning curve is also pulling battery prices down and there are new battery technologies in development, like solid-state lithium anodes, that can keep the momentum going. Falling interest rates can therefore be a positive catalyst without there being a necessary target rate – and it will always just be part of the mix.

Trump vs. Renewables: What’s at Stake?

Q: [Tom] The US election is days away and on a knife-edge. There is a widely held view that a second Trump presidency would be bad for renewable energy. How bad would Trump II be? And how good would a Harris presidency be?

A: [Guinness] Trump has been very open in the last 12 months about his dislike of the Inflation Reduction Act. We see parallels with 2016/2017, where he built that first campaign on his dislike of Obamacare and then tried to repeal it in early 2017. But ultimately, he failed to get that through Congress. He may well try to do the same with the IRA – but we think it’ll be the same outcome. The odds of failure to repeal the IRA are actually higher than Obamacare, because the IRA is pro-growth and pro-jobs – and there’s a huge amount of grassroots support in Republican states because that’s where over 80% of the new investment has gone. You’ve got Republican senators saying they like the IRA. There may be some elements that could be repealed but key pieces like the Investment Tax Credit and the Production Tax Credit stay in place. So if Trump gets in, you will see some volatility the morning after for renewable energy stocks but we don’t think the outlook for them changes hugely. If it’s Harris on 6th November, then we will have a continuation of the way the IRA is moving, rather than any notable acceleration.

The positive in either case is that, a few months on, there will be some certainty on policy and that’s what these companies are looking for before making the next investment.

China’s Influence in Green Energy

Q: [Tom] China is playing an apparently ever-increasing role, both in manufacturing renewable energy technologies and in the scale of its installation of generation capacity. Is China too big to ignore when investing in this space – despite the growing geopolitical risks?

A: [Guinness] In short, yes. China is a huge part of some of these supply chains – in solar, it is 75-80% of the global supply chain. So in that sense, we can’t ignore them. We also think they have some excellent technology. We can debate whether there was unfair use of subsidy, particularly in the early days, but whatever happened, the result now is that China has a lot of these industries at scale, in a way that Europe and the US do not. That drives competitive advantage.

Amid new tariffs, the geopolitical outcome will vary technology by technology. For some technologies, like solar, the US wants to have at least some of its own industry, with companies like First Solar. But, ultimately Washington recognises that China dominating the solar supply chain is probably OK, because solar cells are ‘dumb’ bits of kit. We would contrast that with the higher-tech, higher value-add auto industry. The Western auto industries built up in the 1950s and ‘60s just cannot be let go politically. This is why you see significant tariffs put on Chinese cars.

This protectionist approach probably harms Net Zero goals in the near term – though for some technologies ultimately building out those domestic supply chains is going to be the right way of doing it. Here the US has quite a big advantage over Europe: it can afford to subsidise things like the building of lithium-ion battery factories. Europe doesn’t have the money, so we see more of a compromise, where they allow Chinese products so long as the Chinese manufacturing occurs in Europe. That way the jobs stay in Europe.

For now, Chinese names are around 9% of our portfolio, relative to an historical range of 5-19%.

Public Markets Offer Renewable Upside

Q: [Tom] With plenty of road still to run on the energy transition, how does the opportunity in public markets look today?

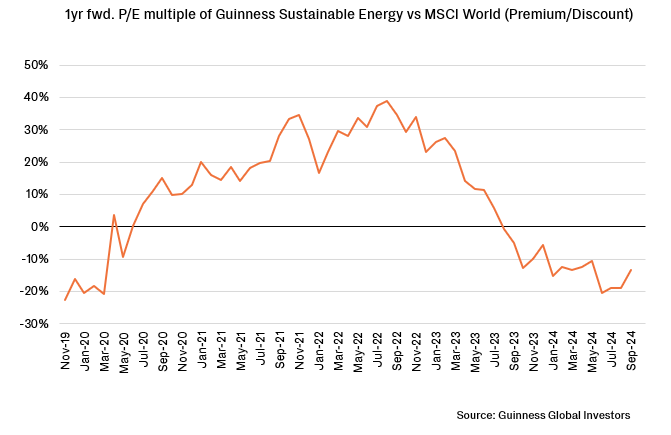

A: [Guinness] Looking back over the last five-six years, we’ve had the pandemic, we’ve had COP 26, we’ve had the EU Green Deal, we’ve had Joe Biden and his infrastructure plans and the IRA. There has at times been a lot of euphoria, pricing in earnings growth that hasn’t materialised for some of the reasons discussed. That disappointment has driven a lot of the money out of these stocks – and they are cheaper as a result.

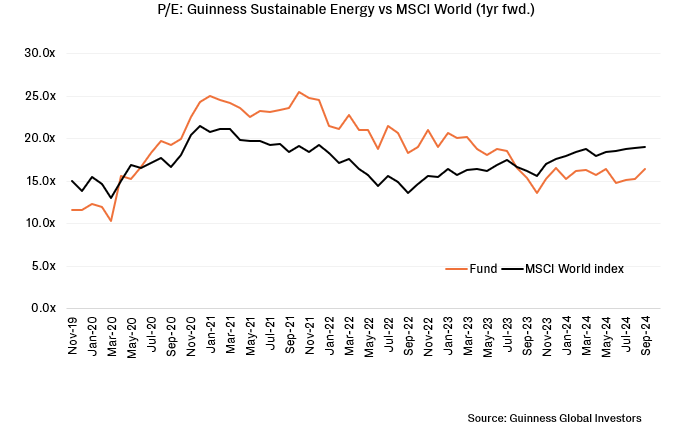

Our portfolio trades on an average 15.6x 12-month forward P/E ratio, versus 18.5x for the MSCI World Index, yet our companies are expected to grow faster than the wider market; consensus estimate earnings-per-share growth is +15.5% for the portfolio 2024-27, compared with just +10.2% for the MSCI World. This is still very much a growth story – but one that is now trading at a discount to the broader market.

Conclusion

From the discussion with Will and Jonathan, there are 3 key takeaways for those interested in investing in the sustainable energy space :

Prepare for a Long-Term Transition: The shift to renewables has just begun – fossil fuels still dominate. Achieving a 50% renewable energy mix by 2050 will require sustained, long-term investment. For investors, this suggests a long-term perspective, beyond the near-term volatility.

Recent Headwinds May be Abating: Some factors that have recently challenged renewable energy stocks are fading – most notably higher interest rates. With rates coming down, investor sentiment on the space may improve. Policy uncertainty nonetheless remains in the US – at least until next week’s election.

Energy transition opportunities are broad – diversify. While solar and wind lead, there is more to investing in the energy transition than these key technologies. Other technologies will play a role – including emerging areas, like hydrogen, that are promising – but face high costs and longer timelines. Investing in the demand side with efficiency and electrification plays is also appealing. Diverse exposure is preferable.

If you have any questions about the themes discussed in this article, please do not hesitate to get in contact with us at info@bedrockgroup.ch

The Guinness Sustainable Energy Fund is not marketed under a UK SDR label, and no formal sustainability claims are implied by Bedrock.

Past performance is no guide to or guarantee of future performance.

Important Legal Information

The content of this document has been prepared by Bedrock S.A., Bedrock Monaco SAM, and Bedrock Asset Management (UK) Ltd. (jointly, hereafter, “Bedrock”).

The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice.

The information contained herein is intended for the sole use of the recipient and may not be copied or otherwise distributed or published without the express consent of Bedrock. Although the information contained herein has been established by Bedrock based on or by reference to sources, documents and systems it believes to be reliable and accurate, Bedrock does not guarantee its accuracy or completeness and assumes no responsibility for any losses that may arise from the use of this information.

Information included in this document is intended for those investors who meet the definition of Professional Client under the Swiss FinSA regulation as well as Professional Client or Eligible Counterparty under the UK Financial Conduct Authority.

Confidentiality

This presentation and the information contained herein are confidential. Each copy of this presentation is addressed to a specifically named recipient and shall not be passed on to a third party. By its acceptance hereof, the recipient agrees to keep the presentation and its contents strictly confidential and may not disclose or divulge any information contained herein to any other person. This presentation cannot be published, copied, reproduced or distributed in any manner whatsoever. The recipient will use this presentation for the sole purpose of obtaining a general understanding of the business, operations and financial performance of Bedrock in order to make a decision as to whether the recipient should proceed with a further investigation of the Funds and this investment opportunity. Bedrock reserves the right to request the return of this presentation at any time, without the retention of any copies by the prospective investor.

Investment Risks

The value of all investments and the income derived therefrom can fluctuate due to market movements and you may not get back the amount originally invested. In the case of overseas investments, values may vary as a result of changes in currency exchange rates. This may be due, in part, to exchange rate fluctuations in investments that have an exposure to currencies other than the base currency of the portfolio. Past performance is no guide to or guarantee of future performance.

Limitation of Liability and Indemnity

Bedrock expressly disclaims liability for errors or omissions in the information and data contained in this document. No representation or warranty of any kind, implied, expressed or statutory, is given in conjunction with the information and data. Bedrock accepts no liability for any loss or damage arising out of the use or misuse of or reliance on the information provided including, without limitation, any loss of profits or any other damage, direct or consequential. You agree to indemnify and hold harm less Bedrock and its affiliates, and the directors and employees of Bedrock and its affiliates from and against any and all liabilities, claims, damages, losses or expenses, including legal fees and expenses arising out of your access to or use of the information in this presentation, save to the extent that such losses may not be excluded pursuant to applicable law or regulation. Any opinions contained in this presentation may be changed after issue at any time without notice.

Copyright and Other Rights

The copyright, trademarks and all similar rights of this presentation and the contents, including all information, graphics, code, text and design, are owned by Bedrock.

European defence stocks have soared since Donald Trump’s return to the White House. In this article, our Research Team explores how European defense equities are gearing up for increased investment and growth opportunities in the evolving security landscape.

This month we discuss the market volatility in March, the new US tariffs—both implemented and announced, developments in the Russo-Ukrainian war, the latest economic data, and the outlook for the almighty US dollar.

This month we discuss the violent equity rotation from the US and growth to Europe, EM, and value, America’s hard-line trade revisionism, falling bond yields, and developments in Ukraine.